Have a question? 720-943-9033

Lights. Camera. Tax Strategy.

Film Production Investments

Unlock Massive Tax Deductions by Investing in Film.

Deduct 100% of your investment—immediately. Own a stake in professionally produced films, reduce your tax liability in the current year, and gain a share of potential Hollywood-level profits.

Program Details

What Is the Film Production Investment Strategy?

This isn’t about being a movie buff. It’s about being smart with your taxes.

Through the IRS’s Section 181, high-income individuals can deduct 100% of their investment in qualifying U.S. film productions—all in the same tax year.

This government-backed incentive was created to promote domestic film production. But for savvy investors, it creates a rare opportunity to:

Instantly reduce your tax burden

Participate in the potential upside of the film’s success

And do it all with minimal effort or industry expertise

Investment Breakdown

Minimum Investment: ~$250,000 (typically a 15% down payment for $1.67M in film IP)

Estimated First-Year Savings:

Deduction: $1.67M (entire investment amount)

30% bracket = $501,000

35% bracket = $584,500

Net Economic Benefit: ~$250,000 in savings over your investment

After fees: ~$212,500 in benefit

Who is this ideal for?

Business owners, high earners, or investors earning $500,000+ per year

Anyone facing a large tax bill—especially after selling a business or cashing in a big gain

Professionals looking for immediate deductions, not slow depreciation

Investors with at least $250,000 to deploy this tax year

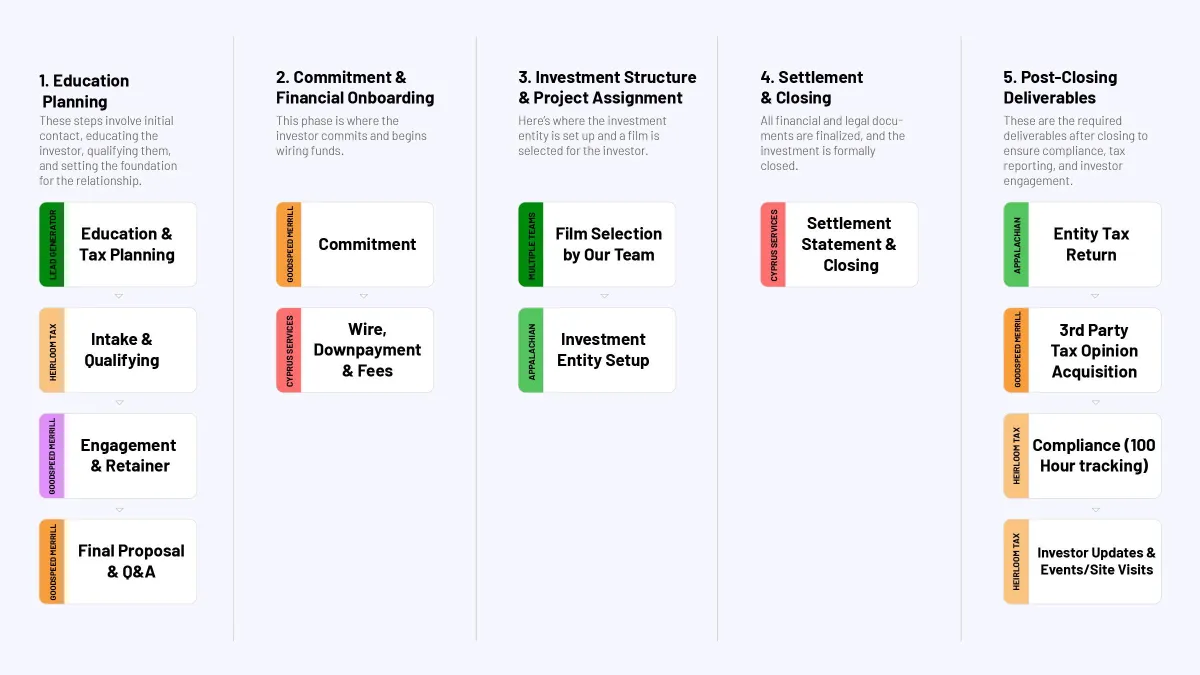

Strategy Overview

PROGRAM DETAILS

How It Works

You invest in a film project as an owner of its intellectual property (IP)—not just a backer. Your down payment (typically 12–20%) secures your stake, while the remainder is financed through structured, IRS-compliant debt.

Step-by-Step:

Choose a pre-vetted film backed by a reputable production team

Acquire a share of the film’s IP, not just production costs

Deduct 100% of your investment amount under Section 181 in the same year

Optionally receive a share of profits if the film performs well

Carry forward unused deductions if needed (offsetting up to 80% of future income)

Important Note: To qualify for full benefits, one day of filming must occur in the same year the deduction is claimed—a detail handled by our team and partners.

Process Overview

Program Details

Why It Works So Well

Why it works so well:

100% Immediate Deduction – No waiting, no phasing out, no depreciation schedules

Section 181 Compliant – Fully legal and built to IRS code

Profit Potential – Earn a share of film revenues, in addition to tax savings

Professionally Managed – No experience required; you’re paired with a pre-approved film and guided by experts

Built-In Risk Protections – Structured funding agreements and legal safeguards mitigate downside risk

Key Benefits at a Glance"

Massive, Immediate Tax Savings

Equity Stake + Producer Credit

Structured & Fully IRS Compliant

Carry Forward Unused Deductions

Minimal Time Commitment

Protected, Vetted Projects

Real-World Example

Let’s say you invest $250,000...

That secures you a 15% down payment stake in a film valued at $1.67 million

You’re eligible to deduct the full $1.67M in the current tax year

At a 30% tax bracket, that equals $501,000 in tax savings

Subtract your $250K investment → your net economic benefit is $251,000

After fees, your take-home savings = $212,500

And you still retain your equity stake in the film

FAQs

If you have additional questions, please book a call with our team, who will be happy to assist.

General Questions

Do I need to know anything about filmmaking?

Not at all. Our team handles all the sourcing, vetting, legal work, and setup. You’re not making a movie—you’re making a smart investment.

Is this really legal?

Yes. This strategy leverages IRS Section 181, which allows 100% of film production costs to be deducted in the same tax year. Our legal partners at Goodspeed Merrill structure every deal for full compliance.

What if the film underperforms?

Your investment is backed by legal protections and structured financing. If a film doesn’t perform, downside risk is limited by revenue guarantees and control mechanisms handled by our finance team.

How much time is required from me?

If you’re using the strategy to offset active income, you’ll need to log 100+ hours of active participation (e.g., reviewing contracts, attending calls). If you’re offsetting passive income, no participation is required.

What happens if I can't use the full deduction this year?

No problem. Excess deductions carry forward indefinitely, and can offset up to 80% of taxable income each year until fully utilized.

IRS Section 181 Questions

How are we billed and why does GM charge based on Net Economic Benefit?

GM wants to incentivize the result and not a larger down payment from the client. This fee arrangement makes the transaction more of a fiduciary fee arrangement.

Fee Arrangement and Circular 230 Compliance

At G|M, we pride ourselves on delivering comprehensive and tailored tax advice intended to optimize our clients’ tax efficiency and wealth preservation goals. As part of our unique service offering, we may recommend transaction- or investment-based tax strategies that we believe will meet your planning objectives and risk tolerances. These strategies are meticulously investigated, evaluated, and structured based on a rigorous and ongoing due diligence process, involving our own resources as well as those of other collaborating advisors, with the goal of generating the best outcomes and client experience.

You will be charged a flat fee for the tax planning and related services described in this engagement letter. The flat fee will be communicated to you after all information regarding your case has been received and analyzed. This engagement is not a contingency fee arrangement, and the fee is not contingent upon the outcome of any tax strategy, the amount of tax benefit actually realized, or any specific result which is ultimately reflected on filed or accepted tax returns. The fee is determined in advance, based on the anticipated value and benefit of the services to you, including but not limited to potential tax savings, the complexity of the engagement, and the expertise required. The fee will not be adjusted or modified after tax filings have occurred.

This fee is not calculated as a percentage of any actual tax savings, refund, or other tax result, and is not dependent on any tax position being sustained by the IRS or any other taxing authority. Rather, the fee is set to reflect the overall anticipated economic benefit of the planning, and is capped at 20% of the estimated Net Economic Benefit (as defined below) to ensure you retain a sufficient return on your investment in these services and the transaction contemplated.

The flat fee also includes amounts that may be paid to third-party vendors engaged by our firm to assist in the planning process. In some cases, a portion of the fee may be reserved to cover the costs associated with ongoing operations and compliance of any structures or entities established as part of your tax planning. Furthermore, any compensation, rebates, or payments received by our firm from third-party vendors in connection with this engagement will be fully disclosed to you. The fees identified in this engagement are estimated based on initial assumptions and recommendations related to the anticipated “Net Economic Benefits” of the planning. Prior to final invoicing, we will confirm these assumptions with your designated financial or accounting advisor. G|M will pay other outside consultants and advisors[1][2] from the fees received in connection with the implementation and maintenance of the strategy, and you will not be responsible for paying any advisors engaged to work with G|M in the development and implementation of the strategies.

Net Economic Benefit and Fee Calculation

The “Net Economic Benefit” will be determined by taking the net value of deductions and credits received as part of the planning (reduced by your investment “cost”), multiplied by 20% (reduced by credits discussed below). This is accomplished by taking the value of the anticipated deductions determined relative to your pre-planning estimated tax rate (i.e., your pre-planning effective tax rate x deductions/expenses arising from the planning), plus any tax credits valued on a face value basis, plus the current value of any depreciation carryforwards or Net Operating Loss (“NOL”) carryforwards based on the pre-planning effective tax rate.

Example:

If you have a pre-planning effective tax rate for the year in question of 33%, and invest $300,000 in strategies and as a result receive $1,000,000 of deductions and $500,000 of credits, then the planning fee of 20% of economic benefit would be calculated as follows:(($1,000,000 x 33%) + $500,000 - $300,000) x 20% = $106,000.

Circular 230 Compliance Statement

This engagement, including the fee arrangement described above, is expressly intended to comply with all requirements of Circular 230 and applicable professional and ethical standards. Under these rules, practitioners are generally prohibited from charging fees that are based in whole or in part on the outcome of a tax position, the amount of tax savings, or the result reflected on a filed or accepted tax return, except in very limited circumstances.

Our fee is a one-time, fixed amount, agreed upon in advance, and is not calculated as a percentage of any actual tax savings, refund, or other tax result. The fee is not dependent on any tax position being sustained by the IRS or any other taxing authority, nor is it contingent upon the outcome of any tax strategy or the amount of tax benefit actually realized. Rather, the fee is determined based on the anticipated value and benefit of the services to you, including the complexity of the engagement, the expertise required, and the overall estimated net economic benefit of the planning, and is capped at 20% of that estimated benefit to ensure fairness and client value.

This engagement letter clearly communicates the scope of services, the method by which the fee is determined, and all inclusions and exclusions, including amounts paid to third-party vendors and any rebates or compensation received by our firm in connection with this engagement. Our goal is to provide full transparency and to ensure that the fee represents a fair exchange of value, is reasonable, and is not unconscionable.

If you have any questions about this fee structure or its compliance with Circular 230, we encourage you to discuss them with us before signing this agreement.

What is included with the Fee?

All planning, project K1 prep for 5 years, Audit defense up to trial for entity, CPA personal tax prep if needed for years in which are impacted, corporation administration, and quarterly investment updates for 5 years.

Will there ever be additional fees due?

No, there will not be additional fees due

Why is the film down payment ½ of the effective rate?

This is to level out the ROI across the project for each investor

How long can NOLs be used for?

Indefinitely

What happens after 5 years to the project?

A decision will be made among the owners of the project based on whether the project is profitable or not. It can be kept and the loan extended if the note is not paid back or canceled out with the producer. If the film is profitable, dividends can continue in its current form, or the film can be rolled up into a more diversified pool of films.

What documents will I have to sign?

Goodspeed Merrill Engagement Letter, Operating Agreement, Agreement to Purchase, Assignment and Attornment Agreement of Film Rights, Assumption of Purchase Money Note, Distribution Agreement, Film Re-Sell Agreement, Purchase Money Note, Tax Opinion Letter Engagement

Is my loan a personal guarantee?

The debt is structured as a loan assumption which has the same legal liability as a personal guarantee. This level of legal responsibility for the debt makes the value of the obligation “at risk” thus permitting the investor to take a deduction for the expensing of the full cost of the film.

How is the investment group structured?

Your investment group will be organized as a partnership in year one. Upon the first dollar of revenue, it will switch to a C-Corp.

Do I recapture income if the note is forgiven?

No, the outstanding note and the IP are placed together into a corporation and offset each other. The corporation is closed out.

Who is actually making the loan?

The producer whom you are buying the IP from is making what is, in essence, a seller-held note.

Can spouses split the required hours?

No, one spouse needs to do the household hours.

How are taxes paid on revenue during project payback?

The revenue received from the proceeds is grossed up by 125% when paying back the loan, so there is 25% to pay for corporate taxes.

How are films valued?

The market values each film. The market can include banks or bonding company underwriting, known resale values for starring or supporting actors in different global markets, genre, directors, and other producers attached to the project. There has never been an IRS value adjustment to the value of a film we have been involved with.

Where does our investment group fall on the mezzanine structure?

Our investment in the 181 eligible portions of the movie for the IP is usually towards the bottom of the mezzanine stack since our investment is leveraged and not paying dollar for actual production costs.

Who provides the K1?

We hire a third-party CPA firm to put the tax return together and issue the K1 to each investor.

Is there audit defense? Who Provides it?

Yes, each entity is provided with legal audit defense up until the need for the IRS to go to Trial. Audit defense is provided by Film Finance Company attorneys from whom we purchase the project. There has never been a need to go to trial and there have been 18 no change audits conducted on these investments as of 2025.

Is this strategy at risk of going away?

Section 181 has been around since 2004. It was not renewed during the Tax Cuts and Jobs act of 2016 but due to an alarming amount of film moving outside the country was reinstated retroactively and extended in 2019 . We do not expect 181 to go away anytime soon.

What happens to income when my film is in the black

The ownership structure flips to 85% original producer, 12.5% investment group, and 2.5% Film Finance Company. Income is paid out as dividends at the corporate shareholder level.

Is the Loan recourse?

Yes, it would not be deductible if it was not.

What Tax Documents do I receive?

K1

Who is my main point of Contact?

Heirloom Tax Solutions will be your main point of contact after intake all the way through project maturity

How will I get and Track my Hours?

Heirloom Tax Solutions provides ample travel and event coordination, film set visits, festival credentials, and online content and readings to help you easily achieve your active hour requirement. We provide you a login to Clockify, a software where we can help you track and document your hours.

When is Money Due?

Both the Down payment and the Fees are due after confirmation of your plan with the Goodspeed Merrill Team and commitment via the signed proposal. Money will be held in escrow until a project, in its entirety, is pieced together and funded.

Who will I be dealing with or receiving documents from during this process?

Goodspeed Merrill, Heirloom Tax Solutions, Appalachian Strategies, Streamline Global, Cyprus Services

What's the difference between a 'Tax Equity Leverage' VS 'Dollar for Dollar' Strategy?

Why would you want lawfirm representation?

Why would you want lawfirm representation?

Should I be concerned about recourse debt?

How do we deal withSection 461 (L) limitations?

What is active participation?

How do we leverage Section 181 and 168 for film?

What does cashflow look like as money comes in?

How do we use NOLs (Net Operating Losses) in a multi-year strategy?

How do we stay IRS compliant?

What protections do I have?

What if the movie does not do well?

How do cash calls work?

How do we make money?

What does advanced mean?

Ready to See If You Qualify?

Get Started Today!

This strategy works best for high-income earners or business owners with $250,000+ available to invest and a sizable tax liability to offset.

Let’s walk through:

Whether this fits your unique tax position

Which projects are currently available

And how to set everything up, step-by-step

Proven Tax Strategies

Renewable Energy Investments

Invest in government-backed clean energy projects and receive substantial tax credits and depreciation deductions.

Min Investment:

$400,000Est. 1st Year N.E.B.:

~$244,000

Film Production Investments

Deduct 100% of your investment in U.S.-based film productions while earning potential revenue from Hollywood-backed projects.

Min Investment:

$250,000Est. 1st Year N.E.B.:

$212,500

Charitable Non-Cash Donations

Donate wholesale assets like medical supplies or educational materials and receive a tax deduction based on the full retail value of your contribution.

Min Investment:

$50,000Est. 1st Year N.E.B.:

$37,500